Estimated reading time: 18 minute(s)

Form 990-T is filed by tax-exempt organizations to report their Unrelated Business Taxable Income (UBTI)–$1000 or more–to the IRS.

Organizations that file Form 990-T should include Schedule A with their main form. This article is an overview of what tax-exempt organizations need to know about filing Form 990-T’s Schedule A and if it applies to them.

What is Schedule A?

Form 990-T Schedule A (Unrelated Business Taxable Income from an Unrelated Trade or Business) is used by organizations to report the income and allowable deductions for each unrelated trade or business they have reported on IRS Form 990-T.

Who Needs to Attach Form 990-T Schedule A?

Organizations that file Forms 990, 990-EZ, or 990-PF should also file IRS Form 990-T with Schedule A–so long as they generate $1000 or more in UBTI from unrelated trade(s) or business(es).

Note: A separate Schedule A should be included for each unrelated trade or business.

How-To Complete Form 990-T Schedule A

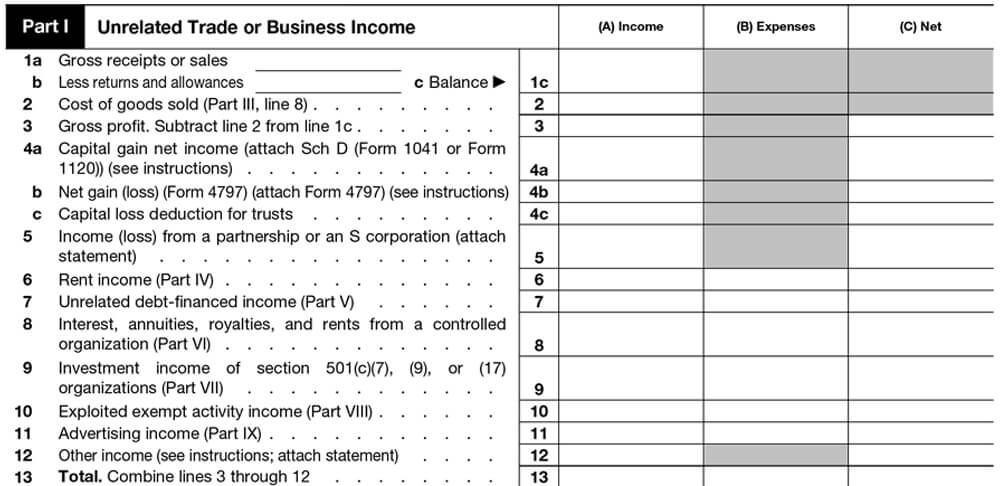

Part I – Unrelated Trade or Business Income:

In this first section, you’ll need to report the unrelated business income generated by your organization in the corresponding tax year.

- Enter the values of gross receipts or sales, cost of goods, unrelated business income, investment income, and others in the following columns:

- Income

- Expenses

- Net Value

- Add lines 3-12 and enter the total income, expenses, and net value.

Note: Trusts should report their capital gains and losses on Schedule D (Form 1041), whereas corporations must report them on Schedule D (Form 1120). If the organization has gains and losses to report other than capital assets, it must report them on Form 4797–Sales of Business Property.

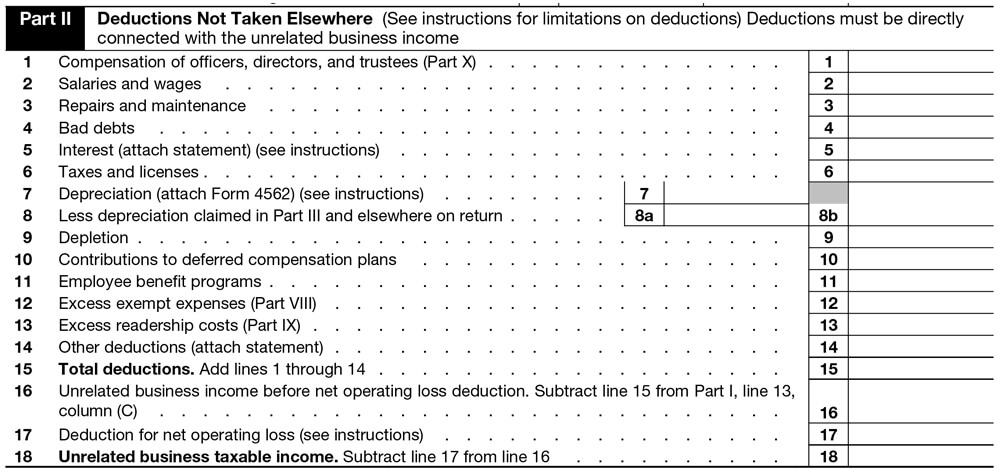

Part II – Deductions Not Taken Elsewhere

If the aggregate sum of the income (part I, line 13a) reported on all Schedule A’s (for Form 990-T) is $10,000 or less, you don’t have to complete lines 1-14 of part II.

- Provide information about the various expenses and contributions that the organization made for the taxable year–including compensation of officers, directors, trustees, salaries, wages paid, employee benefit programs, and other deductions.

- Add the values of lines 1-14 and enter the total deductions. Then determine and report the deduction for the net operating loss. Enter the unrelated business taxable income by subtracting line 17 from line 16.

Note: Both corporations and trusts can file Form 4562 (Depreciation and Amortization) to report other information besides the depreciation value.

Part III – Cost of Goods Sold

This section requires you to report the costs related to the inventory and goods sold.

- Enter the value of inventory at the beginning and end of the tax year, including purchases, labor costs, and other costs.

- Use this information to calculate and indicate the cost of goods sold.

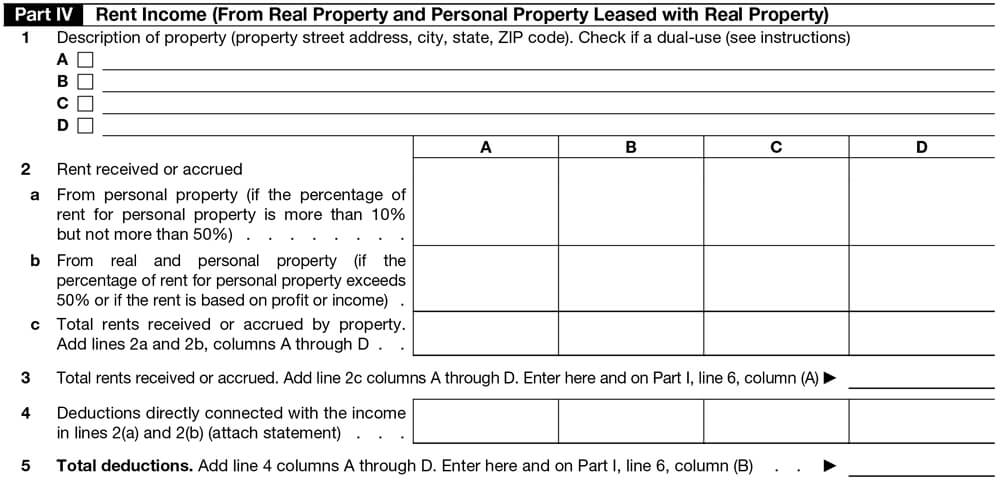

Part IV – Rent Income (From Real Property and Personal Property Leased with Real Property)

All organizations that have applicable rent income (except section 501(c)(7), (9), and (17) organizations) should complete this section.

- Provide details (street address, state, ZIP code) about properties.

- Based on the percentage of rents received or accrued, enter the rents received from personal property, real property, and total rents. Then calculate and report the total deductions.

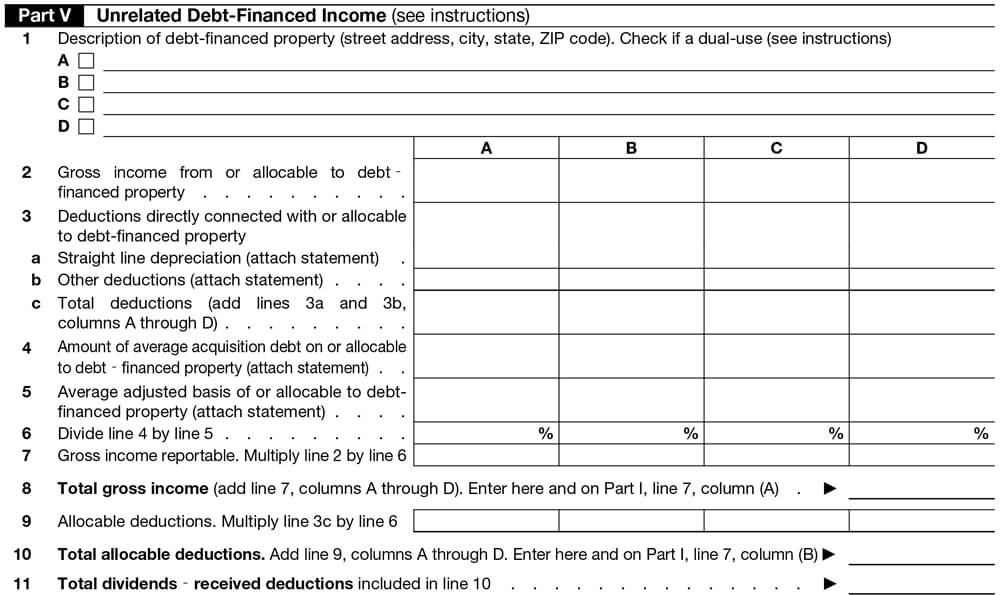

Part V – Unrelated Debt-Financed Income

This part is used to compute unrelated debt-financed income described in sections 512(b)(4) and 514 from debt-financed properties (only when this income doesn’t constitute income from the conduct of an unrelated trade or business and isn’t specifically taxable under other provisions of the Code).

- Provide details regarding the debt-financed properties, gross income from or allocable to those properties, deductions, and depreciation.

- Enter the total gross income, total allocable deduction, and total dividends.

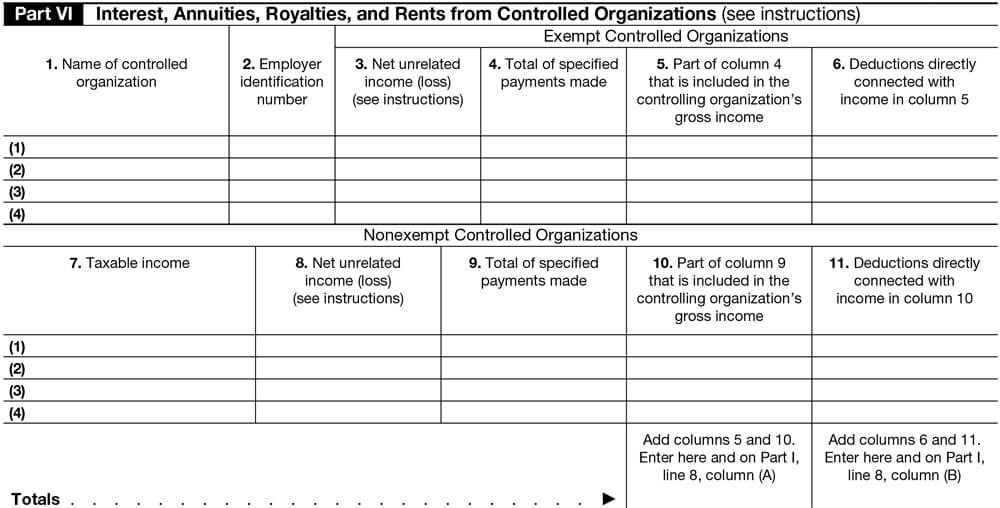

Part VI – Interest, Annuities, Royalties, and Rents from Controlled Organizations

As the name indicates, this section requires information regarding interest, annuities, royalties, and rents from both exempt and nonexempt controlled organizations.

- Provide details regarding the name and EIN of the controlled organizations, net unrelated income, taxable income, and deductions.

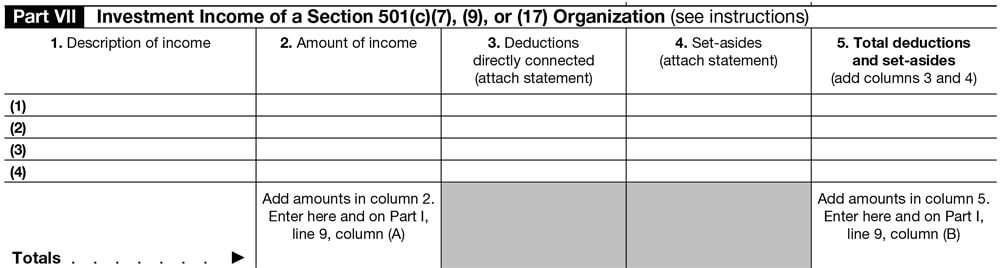

Part VII – Investment Income of a Section 501(c)(7), (9), or (17) Organization

This section requires information about your organization’s investment income.

- Report all the income generate from the organization’s investments in securities and other similar investment income from nonmembers (including 100% from debt-financed property).

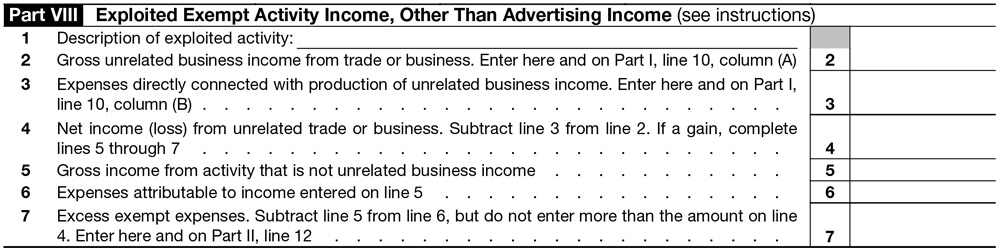

Part VIII – Exploited Exempt Activity Income, Other Than Advertising Income

Exempt organizations with gross income from an unrelated trade or business activity that exploits an exempt activity (other than periodical advertising income reportable in Schedule A Part IX) must complete this part of 990-T Schedule A.

- Describe the exploited activity and provide details regarding the gross/net income and expenses of that activity.

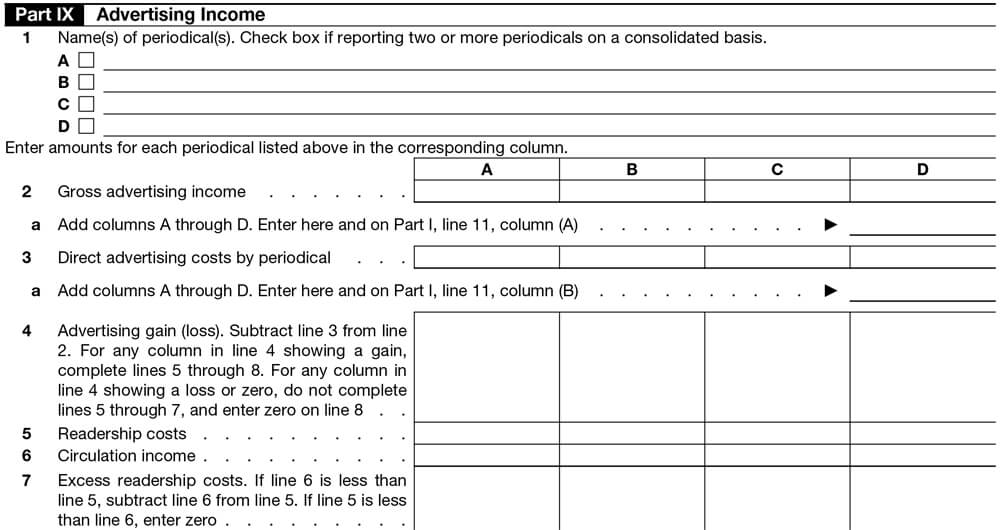

Part IX – Advertising Income

Exempt organizations that generated gross income from the sale of advertising in an exempt organization periodical are required to complete this part.

- Enter the name of the periodicals and report the gross advertising income, advertising, and readership expenses for each.

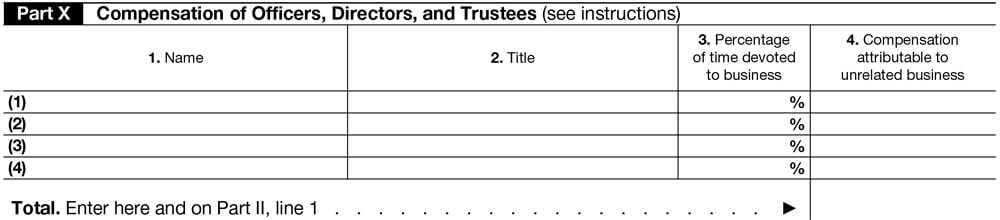

Part X – Compensation of Officers, Directors, and Trustees

This part requires information on the compensation made to your organization’s officers, directors, and trustees.

- Enter the required details about your officers, directors, and trustees–such as name, title, percentage of time devoted to the business, and compensation attributable to unrelated business in the corresponding columns.

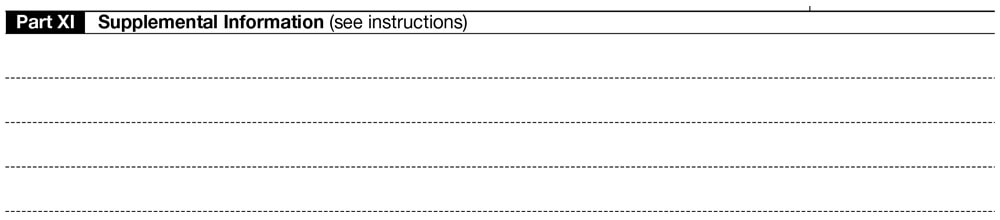

Part XI – Supplemental Information

- This part requires details about your organization’s operations. It also allows you to provide information on lines that don’t have an embedded attachment, information to supplement embedded attachments, and/or any other information about amounts reported on the Schedule.

Note: For example–an organization reporting its unrelated trade or business activity with a different NAICS or Business Activity Code this year than in previous years can use this section to provide an explanation regarding the change.

Looking for the Best Way to File Your Form 990-T?

Get started with Tax990 to quickly and securely file your 990-T with Schedule A attached!

Tax990, the market-leading e-file provider, is the perfect solution for all things Form 990 related–including Schedules!

Here are just a few of the many benefits you can expect when filing with Tax990:

- Identify and fix errors easily using our internal audit check

- Add team members to manage, review, and approve your return

- Schedules are include–at no additional cost!

- Retransmit rejected returns for FREE!

Get started and let Tax990 help you file today!